Bala Srinivasa

“The early part of my career was as a Wall Street Equity analyst covering software in Silicon Valley. Apart from the many lessons of the dot-com boom and bust, it sparked an everlasting fascination with the power of new ideas, and innovation that can transform market spaces.”

“Apart from being an investor, my core skill set is in helping companies scale given my operating background and experience in go-to-market execution.”

The secret sauce for success will be the right combination of Next 400M domain expertise, innovation, and entrepreneurial chops. Founders who combine a deep understanding of Middle India, and leverage technology to design low cost solutions and efficient new business models can build highly differentiated and scalable businesses. We seek to partner with such founders and invest in industry redefining businesses.

Bala Srinivasa was previously Partner at Kalaari Capital, a leading early stage venture capital firm where he backed start-ups across areas such as lending, mobile brokerage, credit scoring, food/grocery and media. Prior to Kalaari, Bala was part of management teams at two successful analytics start-ups where he ran sales, marketing and product functions. His last start-up, Amba Research, was acquired by Moody’s (NYSE:MCO) in 2013.

Bala started his career as a Wall Street analyst covering the software sector in San Francisco. He has an undergraduate degree from BITS, Pilani and an MBA from the University of Toledo.

Building for the 400mn Middle India

The transcript of our chat

How do you define middle India, why do you think it’s such an opportunity area, what’s so special about it? What’s the insight, what’s the size of the market?

When you look at India overall especially as an investor, historically it’s always been India is a billion people, everybody is very young, everybody’s got a mobile phone, after China it’s the biggest opportunity, so you should all be here. It’s a little bit of a broad brush probably worked ok 10-15 years ago, but what’s become very obvious to many of us who are in the investing side or entrepreneurs out there is – there really isn’t one India.

There are lot of faces of India and a vast majority of the first generation of VC funded companies were typically from the larger cities. There are people who grew up in the cities, product you built may be kind of a bit similar to what’s out there in the US or in China and I’m not saying this is true for every company out there, but that’s been the general trajectory of this.

What we noticed is – you had these tech start-ups even from 2011-12 onwards who would scale reasonably, rapidly in the big cities but then kind of hit a wall. That wall took a lot of dismantling in the form of a lot of additional funding – another 30-40 million dollars and really what was on the other side of the wall was a market segment that thought very differently, had very different pricing points, had very different consumption habits, affordability risks than the top three metros or the top ten metros.

Satya Nadella just talked at the Carnegie Institute Conference. He talked about how he wants the India stack which is the Aadhar and the e-KYC and UPI to be taken global. But in 2014-15, it was just beginning to come online and we felt there was something magical happening where three of the biggest barriers to middle India maybe coming down. There is now a door-way into middle India.

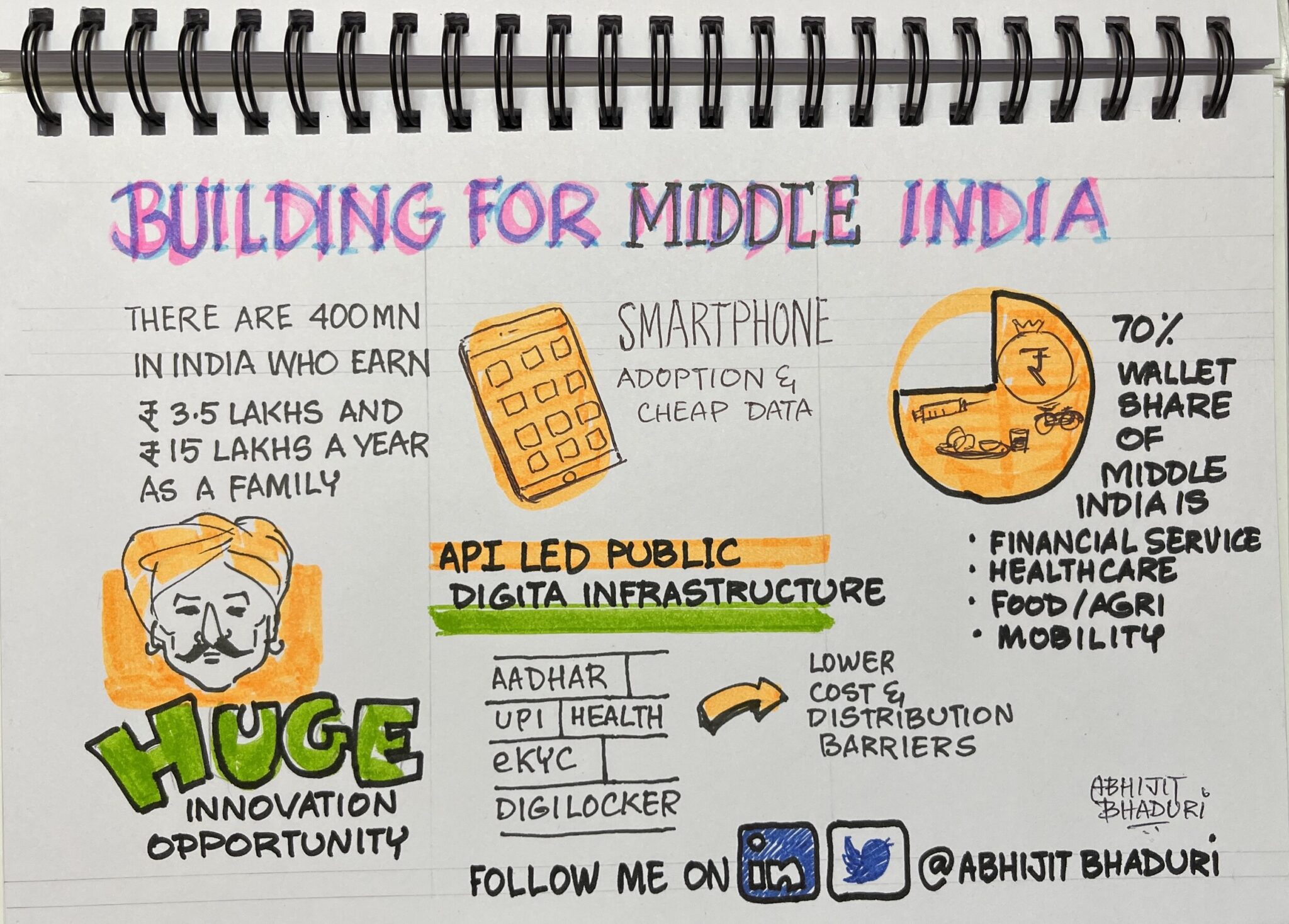

The hardest thing about middle India historically which is about 400-500 million people, the way we define it is – people who make between 3 lakhs and 20 lakhs in family income. I’m not saying per capita GDP, I’m saying family income. Those people form a very large segment in India but they are not poor by Indian standards.

I’m not talking about the 500mn at the bottom of the pyramid – less than 2 lakhs a year. I’m not talking about the top 10 million families that are above the 20 lakhs a year in family income category.

>

“I’m not talking about the 500mn at the bottom of the pyramid – who make less than Rs 2 lakhs a year. I’m not talking about the top 10 million families that are above the Rs 20 lakhs a year in family income category. ”

In middle India are folks were 98% of them for example shop at the Kirana store. They don’t go to Reliance Fresh for example. 90% of them don’t have health insurance, 80% of them probably don’t have more than 1 debit card, may not have a credit card. So, there is very large mass of people who have affordability but even historically brick and mortar companies have not been able to reach them because of 3 things, that is:

-

There is the cost of customer acquisition, of acquiring a customer

-

There is the cost of transaction which is doing business with them

-

The risk of transaction (which is if I give them credit for example and I start doing business with them, are they even going to repay me back?)

>

“HDFC has 40 million customers after 25 years in India. There’s a reason for that. The reason is they don’t think from a business perspective it’s economical for them to go after middle India. ”

We felt now the time is right with technology, rails that are in place for entrepreneurs who can combine technology with solving complex problems in certain verticals – I’ll come to that in a minute and being able to rethink business models with a fresh sheet of paper which we’ve always learnt – it’s very hard for an existing large company to change direction because of their shareholder expectations, the way they have brick and mortar offices everywhere. But we think this is an amazing time if you’re an entrepreneur in India and not necessarily tech, to be able to offer essential services much more efficiently to these next 400 million Indians on the backbone of technology rails that are being built in India. So, that’s really our overall thesis and we’ve built an entire fund around it because in our past funds you would do a very broad range of sectors and a very broad range of ideas – it could be jewellery, it could be fashion commerce, it could be financial services, it could be anything. But we feel, just focusing on innovation for middle India, there is plenty of opportunity and we could find the next, really large, big success stories in India by doing this.

When you think about middle India, one of the questions that would be there is – you are essentially an urban person – the people who are building it are building it in Bangalore. How likely is it that they even understand the needs of middle India unless you’re from there? How do you solve that problem?

If you look at many of the second time, third time founders in India today and I will say a lot of what we do is tech oriented, it’s not necessarily tech – many of them are from Tier 2 towns or Tier 3 towns. They’ve all had a good education, many of them have gone to BITS, they’ve gone to IIT, but they’ve gone to a very good regional college, but they’ve now migrated to the cities and a lot of them have an inherent understanding of what middle India looks like.

I’ll give you an example – one of our investments is a company called Krazybee – led by Madhu who is the co-founder there. The Krazybee product is a product you would never use. So the product is a small ticket loan where they’ll give you a loan between 2000 rupees and say 15000 rupees if you will and this loan solves a problem that again you wouldn’t have which is most of middle India is like I said earlier, is not poor, but they have a cash flow problem which is, you might end up in June timeframe with 3 kids whom education needs to be paid.

You might end up with a health care emergency for a parent where you don’t have extra cash in your bank. So, this product that they’ve designed, one of the things we look for is – if this is a product we very instinctively use, we sometimes feel we’re barking up the wrong tree. And most of these founders are founders who come from not necessarily the big cities, who have very good sense for how this product works and he’s designed this product which has scaled very very rapidly in 4 years. They are doing a million loans a month now. They’re able to do this on the back of this technology rails I talked about. They can disperse a loan in 15 minutes flat and this product itself wouldn’t have existed 5 years ago because you didn’t have the infrastructure.

So, you look for this inflection where if you came 7 years ago and said that I want to build a product like this, you wouldn’t, because there was no way to reach these people in terms of digitization etc. And so most of the founders we work with like Jumbotail is a company in the Kirana store business that we are investors in, while Ashish must have gone to Stanford, he’s actually from Himachal Pradesh, his parents are apple farmers over there and he’s got a very good sense for how it works, but you’re right, overall there is still a bias in the VC business and the technology business where you end up seeing more and more entrepreneurs in the larger cities. But if you really want to build a company on a product like VR for middle India , we spend a lot of time to sus out whether the entrepreneur completely gets it through various reference calls, etc. etc.

You talked about Fintech, one of the things, the way it has gone in Africa for example – there’s a huge population which is unbanked and that is a massive fintech opportunity. In fact one of the things A16 Z talks about is every company is a Fintech company in some sense or the other. Does this model change when you move sectors? In healthcare, the delivery system is so fragmented, does that make it impossible to solve some problems and are some problems safe? Fintech is easier to solve than say education or healthcare. How would you view it?

Actually, the problems are on equal footing in the sense that they’re massive, complex and not easy to solve because of precisely what you mentioned. The way we look at it is – if you take healthcare, we’ve invested in a company called BestDoc – it provides a SAS platform for hospitals. Based on IBF data that we have seen, India has supposedly pre-billion hospital visits – out patient hospital visits every year and about 50 million hospitalizations. And most of these hospitals are in Tier 2, Tier 3 towns, exactly like you said which is very very spread out. And part of the challenge in a country like India which is true for Fintech as well is, it is very very difficult for you to put feet on the street and physical presence trying to solve for this. But that does not mean every problem can be solved digitally. You can’t say that if a person’s going to need heart surgery, you haven’t reached that stage today but atleast robotically you’re going to do something, but the next best thing you can do is to use technology to provide for something – cardiac, telemedicine but also on a more serious level being able to not just see a doctor, being able to review an ECG, or being able to review an EKG or EEG centrally – that’s one example.

But same thing is in Fintech. The biggest challenge in all of this is – can you build a product? We had Sachin Bansal (after Flipkart he is building a financial services). He said something very interesting which we believe in which is – the single biggest problem that we are trying to solve for middle India and he’s also really trying to solve for middle India is – while everybody’s got a smartphone, you really want the product to be so simple that people adopt it and that is one of the biggest design challenges for any of these sectors today.

So, 70% of middle India’s wallet share is actually only 4 areas – financial services, health care, the food that they put on the table – food and agri, mobility and education – 5 sectors and we actually focus on the first four. 400 million people are there, aggregate them, they’ll spend a lot of money. The challenge is, can you design something different where it is easy for them to adopt it and you can still make money and you’re solving a problem. So, it’s very high bar, it’s not easy to do. The one’s who do will really find some amazing outcomes on the other end.

When you look at this kind of landscape that you’ve painted, there is a certain degree of complexity – there is no two ways about it even if you’re from middle India or if you’re from rural India – below that. It’s still a fairly complicated thing because India is so hugely diverse – people from one region find it difficult to understand the nuances of the neighbouring state. What is your method of really trying to get consumer insights? Where you identify white spaces, opportunity areas? What is your method of getting a first-hand view because I could come back and tell you – here is a problem I see, how do you know it’s right or wrong, how do you access an independent view of that?

That’s a good one. We are in the long-term business.

Define long-term for yourself?

Our investors give us capital that has a ten-year life. We need to give them outcomes starting maybe year 7, sometimes it can stretch even beyond 10 years. And the reason Venture Capitalist is an asset class that is different from public markets fir example is, we are in the early stages, we are not seed investors but we look for an entrepreneur with an idea in our case. We are looking for customers with some foot/toe in the water in terms of what you say your product will do.

We are still very early, we may invest in year 2 of a company’s existence. We are primarily going with our belief in the entrepreneur. Everybody’s got their own mental model and for our mental model is – are they able to articulate what they are reimagining this space/product. How it’s likely to look 5 years out. You’ll be surprised how the top 1-5 people really stand out. It’s very much possible as they go through – they make pivots, they make changes, but these are people with tremendous amount of confidence in how the market will change.

I’ll give you an example, Madhu at Krazybee, first time I met him I said no because his original idea was – I’m going to use these digital rays and I want to give student loans in India. This was too complex and we didn’t want to do anything. But what we saw was, within 18 months they were out in 75 cities in India. The top 80 million Indians live in the top 8 metros that is another 74 million Indians who live in the next 40 cities. But once you pass the 40 cities, you live in cities with less than 1-2 million population. They became the number 1 lender to students in just 18 months. One of the things you do is stay in touch with people like Madhu, because you want to know how are they doing this stuff.

Then you follow-up and get to realize the best is betting on Madhu because I don’t have the ability to imagine the space the way he does. We stayed in touch with him and we got the opportunity to invest in him and we were very happy. So, we are first looking for the entrepreneur, but middle India, given the wallet share example I gave, automatically creates a filter for the largest market spaces – there are no bigger marketspaces than these 5 sectors. If you cross the entrepreneur, we are looking for, who checks the boxes for us. We’ve got around 15 parameters, we like to think about them, with these 4 largest you’re in a reasonably good space because we’ve consciously said we are not doing gaming. Not than gaming is not a big area, potentially it could be a big area in India.

Is there a particular reason why you wouldn’t do Gaming, given the fact the e-sports is a 160 billion $ industry?

We are trying to invest in 15-18 industries in this fund. We feel that 4-5 sectors as large as what we have are going to be sectors where we like to focus on, we’re also looking for sectors with exits. When we have to give money back to our LPs, we also want a situation where these companies increasingly, we see what Reliance is trying to do, you’ve seen what Tata’s have done with Big Basket. For the first time in India, you’re seeing large conglomerates view new start-ups and innovations as a place where they want to pay premium. These big sectors where large corporations today see disruption, see the way their business might change are areas which are more likely to see exits. It’s not the only way to do it, that’s the way we’ve chosen.

What are the myths of middle India that have proven to be wrong?

>

“The biggest myth we feel is that you can’t make money selling to middle India”

You can’t make money if you have the top 8 metro mindset. What we have found is if you can solve for the 3 things – the cost of customer acquisition, the cost of servicing the customer and manage the risk to servicing the customer – suddenly brand new avenues open up. Almost every company we are investing in now is unit economic positive either from day 1 or very near future.

These founders are executing what we expect them to execute which is to understand middle India. Our product only has value if it’s value proposition to this audience – making 3 lakhs to 20 lakhs per year is at a price point they will consume at a frequency that is valuable to them but where we can make money. The three things that we are looking for is – it’s a very high-volume product, there’s frequency of usage by the consumer, because of frequency of usage, drives faster turnover in the service provider and if you’ve got your margin structure right, you can make lots of money by doing lots of small transactions.

When you have a portfolio of companies, what is the ratio of failure and success. Is it different if you would not focus on middle India and if you would do it for an urban consumer, would it be a different success rate?

There’s been one global study done across all VC markets which I think is a gold standard study. What happens is you pick your own target market. But in any given fund, doesn’t matter who it is, you’ll find that there are about 2-3 companies that drive 90% of the outcome of the fund. Top 10 companies will drive 90% of the outcome. This is why VC is a different asset class. When you invest, you feel awesome about your companies, but you also know the mortality percentage. So we are expecting 2-3 companies are going to take off like a J curve and by the 3rd or 4th year if 3 companies do more than a 9x or 10x, your goal in terms of outcome as a fund you’ll expect another 2-3 companies to be between a 5x and 9x in terms of outcome. This is over a ten-year period.

You have a third of your portfolio that simply doesn’t make it where you’re lucky to get your money back. The reason this model works is you know your risk profile; you’re not trying to invest in a business that is going to provide very predictable outcomes. We’ve been asked to invest in innovation that can really change marketspace and provide outcomes. The greater amount of satisfaction for me is these young founders are changing the industry with their ability to take a lot of risks. The great companies are the one’s that go beyond the idea and technology into building very lasting company cultures, lasting teams and being able to onboard different levels of talent and bring it to scale.

Which is very close to Dreamers and Unicorns – any responses?

The comment you make about – if you think about any new business as a purely digital business, you’ll be doing yourself a big favour. We have companies that start out with a technology idea but you’ll find that you have to plug holes that may require a call centre. That central idea of the book was a powerful one, in almost all-out companies, we see our founders think that way. For us it’s always a red flag if we hear somebody who says ‘we understand this entire thing, we got all the processes. Now we’re building technology to automate a series of these processes. Nothing wrong with it, but for us it doesn’t work because historically it has never scaled given the barriers, we talked about for middle India

Do you see more start-ups succeeding when you have more than one founder, it could be a single founder? What is the average successful founder’s profile?

In my last firm we did a study which is on my LinkedIn profile with all the data which will answer most of your question. One belief is that all founders are very young and are from IIT’s and Biz and they are the only ones out there. There is some amount of truth in it, but there are some of the companies founded by people who are more than 70 years of age. About 50% of start-ups that get funded are not necessarily from founders who are from IIT or IIM. There is a propensity for VCs globally and if you look at global success stories, they are primarily driven by young founders and lot of that has to do with your ability to take risks.

Someone whom I’m very proud of is a very young BITsian who runs a company called Pixel, they are in the space technology start-up. Just his level of thinking of wanting to run a nano-satellite, he’s basically out of college. He already got a ride through ISRO, PSLV. He’s all of 23 years. The biggest thing while talking to somebody like him is that they have no fear of failure which is a very big checkbox. As you get older, the memories what you call experiences can end up becoming a failing down the road. The really good young founders understand their experience gap and bring in people who can fill them.

Lot of start-ups use cash burn for promotion, is it justified?

Totally depends on the product and the company’s business model. Many of the companies don’t advertise at all. The example of Jumbotail which is supply-chain for kirana stores, even today doesn’t advertise. It’s totally viral – word of mouth. It’s the best kind of promotion. It tells us two things – the value proposition of your product is good enough where people are adopting it on their own. Second, more B2B and B2B-C companies have less need for cash burn for promotion, but if you’re a pure B2C start-up and if you’ve not managed to crack any viral adoption, you may have no choice but to invest a meaningful portion of your budget to get noticed. In case of Krazybee, the product is truly viral. It comes from the strength of the product.

In India, literacy rate is very low. How do companies go about communicating their ideas? How does it work?

There are only about 200-220 million English speakers in India, 1/5th of the total population which is 12 years and above. What is very exiting is, this is the first year that rural internet users in India have crossed the urban crowd. It’s about 227 versus 200. The smart founders find ways to design their products. Our thesis is called Middle India by design. We think the design of your product is the biggest element of your success. Jumbotail, they are talking to kirana stores people who they don’t touch, it’s a viral app. The way the kirana stores guys interact with the app with a lot of stickiness is because they use a lot of pictures, certain bundling of products which are familiar when a local distributor comes, it’s very pictorial. Start-ups are doing a very good job of vernacular based offerings. In the B2B side start-ups are using building deep tech to help other start-ups to reach middle India vernacular dialect-based language. There are others who are building the product completely non-English, vernacular language and going state by state, language by language and trying to solve for it. It’s a very big opportunity, but it’s a non-trivial challenge to try and win.

Would there be a product equivalent to LinkedIn for middle India which creates these jobs? One of the theses in the book is potentially the next set of jobs is pin code based, is that going to be the next thing that’s going to happen in the job market? Is that a valid thesis?

It’s a valid thesis. India has some over-arching issues to solve for, one of which is jobs, especially for 700 million people. There are 3 ½ thousand small towns and villages where half the population of India lives, these people are all migrating to cities. This youth population needs jobs. There’s a lot of push by the government both through talking and through many programs to try to move entrepreneurship along. The challenge is, most of these people have other challenges which are infrastructural. We think that one of the big drivers of jobs going forward is going to be eco-systems driven by some of the entrepreneurial activity that we are talking about. If you were to take somebody like a Big Basket and you go to their warehouses across, you will find that whoever has been employed there is now all of a sudden exposed to something like a bar code. The same thing applies to an Ola or a Uber where you’re taking somebody into a more organized business. The challenge in India is there are very very few formalized businesses. These 40-50 million Indian small businesses are all informal by and large. Nobody ever scales to become informal. If we see more and more innovation for middle India by companies for middle India, you would hope to start seeing formalization of new age businesses whether it is around vernacular based stuff or it is around new age eco systems that can drive more jobs at which level something like LinkedIn for middle India would make sense. LinkedIn is essentially a white collared job market. I don’t think that homogeneity is there for middle India LinkedIn in my view, but it will change.

What is it you predicted is December 2019 which is still valid about the market? Beyond the pandemic, what did you get right and what did you get wrong? What is your prediction therefore for 2021?

On the personal side, I start off the year wanting to do a lot of different things. I’ve been wanting to play the guitar for a few years now, I had a list of 20 songs to get to. I’m probably somewhere around 8 or 9. The number of books you want to read, all that is fairly typical. As a fund, it’s actually worked out. We were very fortunate, we got to a first close in February this year. It was delayed from August last year, but we are still very grateful that we were able to get through right before the pandemic, another couple of months and we would have struggled. Nothing much to complain about. My list of things of we do wrong are way longer.

One prediction for 2021?

What we are seeing on a daily basis is the digitization of India and the acceleration is going to surprise everybody next year when everybody comes out of Covid because you just look at what this crisis has just done in terms of people’s willingness to use technology everywhere, all around, from older people to younger people, to government, to banks, to institutions. In hindsight, this may turn out to be that inflection point that we’ve all been talking about and projecting, but didn’t know when it would come.

What is an unmet need of “middle India” you would like to see addressed? Leave your idea in the comment below